Categories

all

Banking

Posted: April 15, 2024

The digital age has brought us many things: social media, e-books and streaming services. It’s also changed the way we live our lives, from online shopping to food delivery apps, GPS directions to virtual meetings.

One of the most significant—and convenient—innovations of our time is online banking. Online banking has evolved from checking your balance online to connecting bank accounts, whether they’re at the same bank, different banks or third-party apps. The goal of connecting your accounts is to make it easier for you to manage your money, but many people still have questions about the security of linking accounts.

Linking accounts at the same bank

It’s not uncommon to have multiple accounts at the same bank, e.g. checking and savings. It’s simple to link these accounts on your bank’s website or app and makes it easy to transfer funds from one account to another. Some banks also provide incentives for people who link these accounts, like waiving monthly maintenance fees or overdraft fees.

Linking accounts at different banks

Some people maintain financial accounts at different banks; for example, they may keep their checking at one bank and their mortgage at another. It is possible—and perfectly safe—to keep accounts at separate banks but link them so you can easily move money between them. Many banking sites allow users to check information for both accounts in one place, but may have processes in place regarding how transfers can be made.

Linking accounts to third-party apps

Third-party finance apps like Venmo, Zelle, Cash App, PayPal and PocketGuard offer consumers alternate ways to manage their money, whether it’s to transfer money or track and manage spending. Though these apps are secure and safe to use, they do access sensitive information like bank account and credit card numbers. They don’t have the same kind of secure backing found at banks, but some are protected by the Electronic Fund Transfer Act, which protects consumers against unauthorized transactions.

Before you connect a third-party app to your bank accounts and credit cards, do your homework. Make sure the app is reputable and offers protection against unauthorized transactions.

How to link accounts

Linking accounts at the same bank is typically done automatically and simply requires a single sign-in to your bank’s website. Linking external bank accounts requires additional information and may vary by financial institution. In general, it’s smart to follow these steps:

- Gather relevant information, like account numbers, routing numbers and logins.

- Log in to your bank’s website or app and find the option to link or add an external account. The option may be on the dashboard or in settings.

- Select or type in the bank or financial institution you want to link.

- You might need to log in to the other bank you’re linking.

- Complete the verification process, usually sending a small deposit to confirm the accounts are linked.

The safety question

So, is linking bank accounts secure? Banks and credit unions utilize a variety of features to ensure safety, including:

- Transport layer security encrypts data, preventing hackers and cybercriminals from accessing your personal and account information.

- Tokenization involves exchanging data by converting it into tokens, which hide private information.

- Multi-factor authorization requires users to verify their identity using a numerical code sent to via text or email, PIN, fingerprint, or facial recognition.

Even with these safeguards in place, it’s important to take precautions when it comes to sensitive information. Keep passwords and PINs private, use two-factor authentication whenever possible, and research third-party finance apps before linking your accounts.

Still have questions? Contact us for more information.

3 minutes read

3 minutes read

Finance

Posted: April 9, 2024

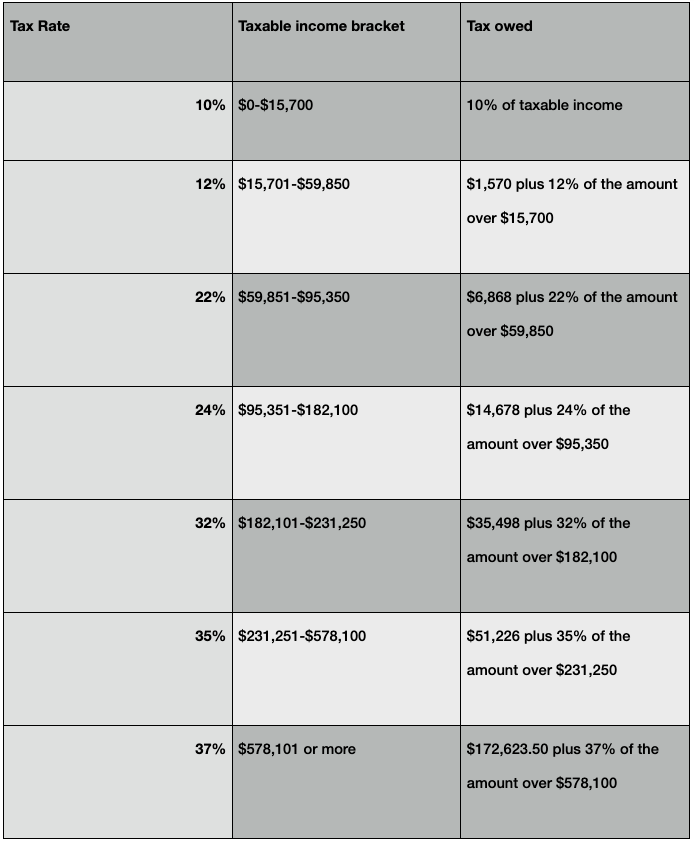

As tax day approaches, it’s important to understand the different tax brackets and what that means for you. Your tax rate is determined by your taxable income and filing status, which will drop you into one of seven tax brackets for 2023. Each bracket is assigned a corresponding tax rate; the highest rate, called a marginal rate, only applies to a portion of your income (more on that later). This system means that people with higher incomes pay higher federal taxes, and vice versa.

Federal rates will remain the same until 2025, thanks to the Tax Cuts and Jobs Act of 2017; however, the IRS may adjust thresholds for inflation.

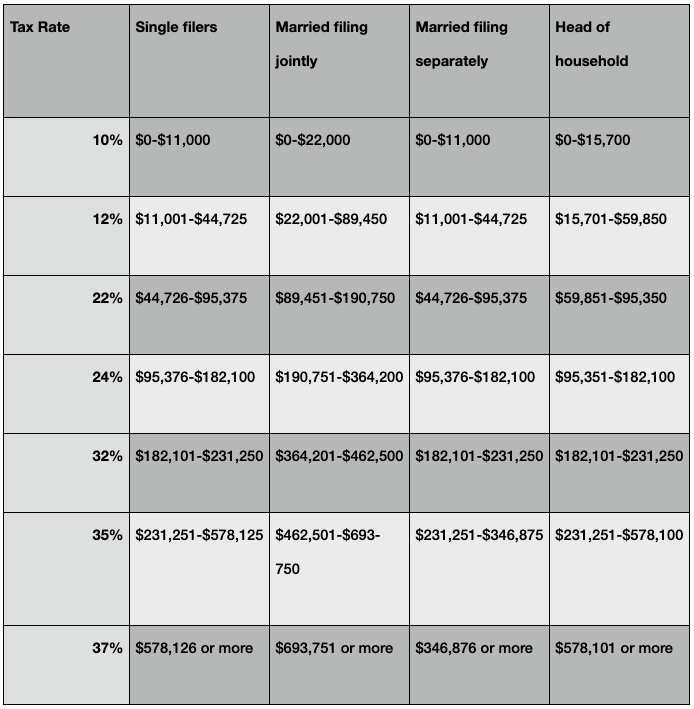

2023 Tax Brackets

There are four main filing statuses when it comes to taxes:

- Single filers

- Married filing jointly

- Married filing separately

- Head of household

Your income based on these filing statuses will determine your overall tax rate for the year.

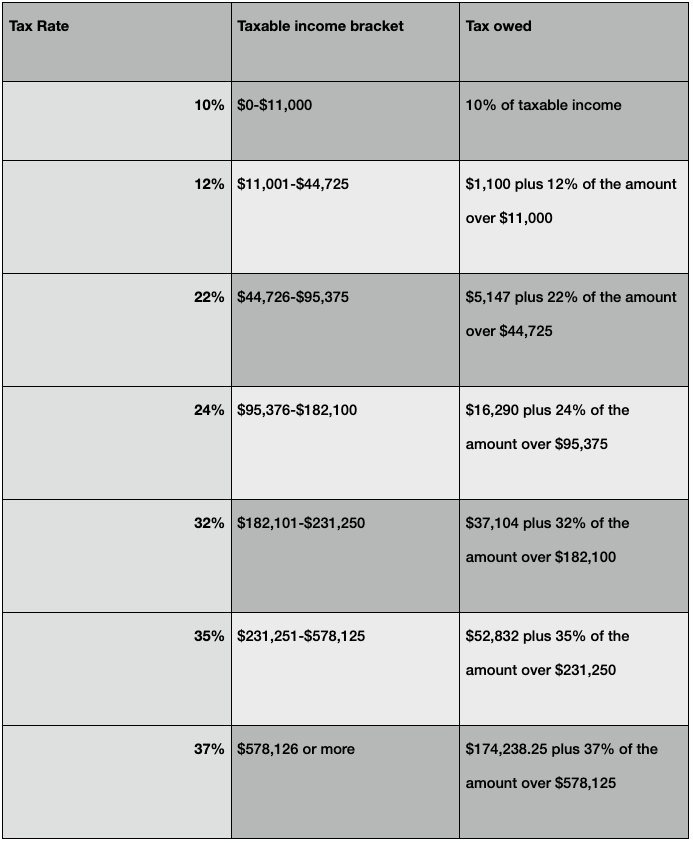

For example, a single filer who made $50,000 in 2023 is in the 22% tax bracket. However, to complicate (but improve!) matters, this person won’t pay 22% on their entire income. Instead, their tax breakdown will look like this:

- $0-$11,000 of their income is taxed at 10% (approx. $1,100)

- $11,001-$44,725 of their income is taxed at 12% (approx. $4,047)

- $44,726-$50,000 of their income - only $5,274 - is taxed at 22% (approx. $1,160; this is the marginal rate)

That adds up to a tax bill of $6,300 ($5,147 plus 22% of the amount over $44,725), or 13% of this person’s taxable income - even though they are technically in the 22% bracket.

So, what is that 13%? The 13% is called an effective tax rate, which is the percentage of taxable income that you actually pay in taxes. To calculate this more easily, divide your total tax owed (line 16) by your total taxable income (line 15) on your Form 1040. The charts below can help give you an idea of what you owe.

Single filers

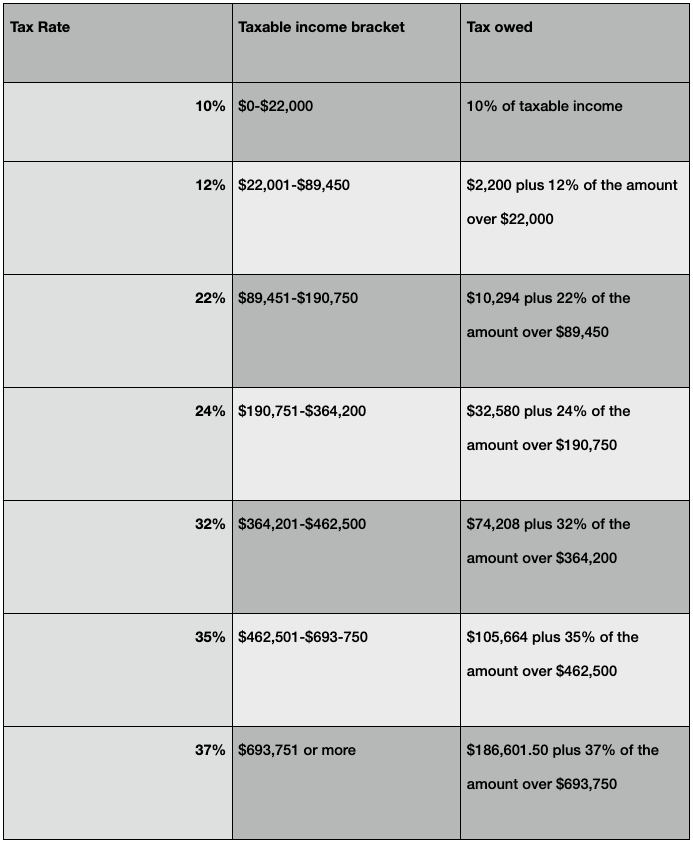

Married filing jointly

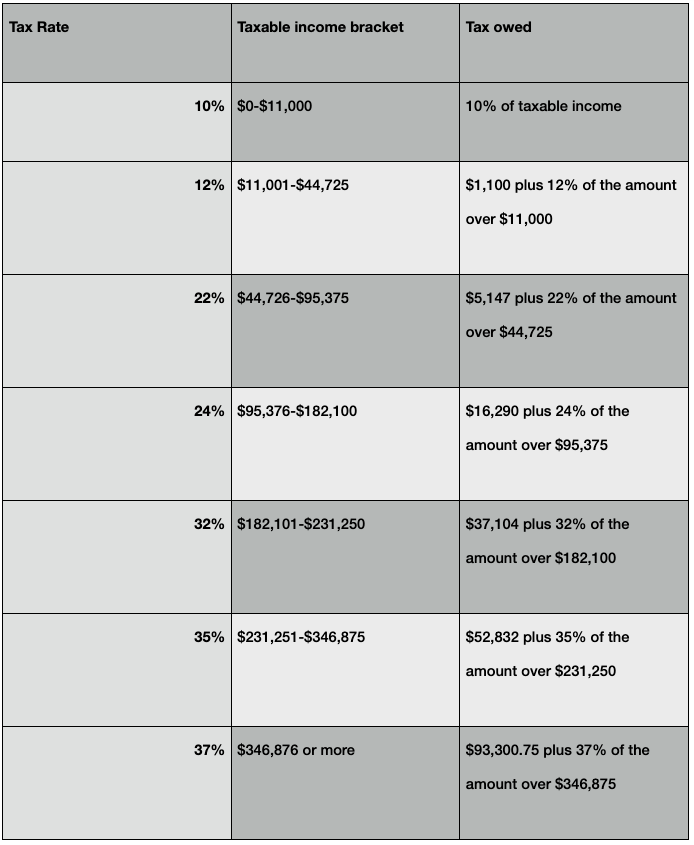

Married filing separately

Head of household

Reducing taxes owed

Finally, there are two ways to reduce your tax bill: credits and reductions. Credits reduce your bill on a dollar-for dollar basis and don’t affect your tax bracket. Deductions reduce how much of your income is subject to taxes. Check out our Delving into Tax Deductions blog for more info!

5 minutes read

Finance

Welcome to the world of financial literacy, where the right information can transform your relationship with money and set you on the path to success. In this blog post, we will be reviewing five of Amazon’s top-selling finance books, because whether you’re a seasoned investor or a financial newbie, you can always learn something new. These books’ invaluable insights are reader-approved to help you reshape the way you think about and manage your money.

- The Simple Path to Wealth by J.L. Collins

Author and financial expert J.L. Collins provides a straightforward and practical approach to achieving financial independence in The Simple Path to Wealth. The book emphasizes the power of long-term investing in low-cost index funds and addresses common pitfalls, such as debt, that can hinder financial success. Collins’ conversational style and relatable anecdotes make complex financial concepts accessible to readers of all levels of financial expertise.

- I Will Teach You to Be Rich by Ramit Sethi

In this comprehensive guide that covers everything from budgeting to investing, Ramit Sethi combines financial advice with a touch of humor, making it an engaging read. The book focuses not only on building wealth, but also encourages readers to define—and then design—a rich life for themselves by aligning their spending with their values. Practical and action-oriented, this book is an excellent resource for those looking to take control of their finances.

- The Millionaire Next Door by Thomas J. Stanley and William D. Danko

More than four million copies have been sold since this book was published in 1996. Although the societal landscape looks very different today than when the book came out, the fundamentals behind Stanley and Danko’s research into how ordinary citizens become millionaires remain true. The authors’ deep dive into the habits and mindsets of the “next-door millionaire” reveals that living frugally while prioritizing saving and investing are behaviors that contribute to long-term financial success.

- The Psychology of Money by Morgan Housel

When it comes to money, what you know isn’t as important as how you behave, argues Morgan Housel. Attitudes shaped by experience and societal expectations can play a key role, as Housel shows in this exploration of the different—and often irrational—ways that people deal with financial matters. Anchored by 19 short stories, The Psychology of Money provides a look at the strange outcomes that can result when thoughts and feelings collide with logic, belying the school of thought that finance is purely a numbers game.

- The Intelligent Investor by Benjamin Graham

Regarded as a classic in the world of investing since it was first published in 1949, The Intelligent Investor remains widely acclaimed for its timeless principles for wise investing. Benjamin Graham’s insights, adapted for modern investors by financial columnist Jason Zweig, emphasize the importance of a disciplined approach to investing.

Remember that financial education is an ongoing journey. Each of these books adds a unique perspective to your personal finance bookshelf; together, they form a wide-ranging collection to guide you on the way toward achieving financial well-being. Visit your local WaterStone Bank branch to speak with a banker and find out how we can assist you on your financial journey.

4 minutes read

Finance

From essays to applications, there is a lot that goes into preparing for college. Chief among them is the Free Application for Federal Student Aid, or FAFSA, form. It’s smart to complete the FAFSA form as soon as it’s available, because federal funding is limited.

What is FAFSA?

FAFSA is an application for federal student aid, including federal grants, work-study programs, and loans, for prospective and current students. Some states, colleges, universities, and private lenders also use information from FAFSA to determine students’ eligibility for financial aid. You must complete the FAFSA form for each year you plan to apply for federal aid.

Information reported on the FAFSA form is used to calculate the student’s Expected Family Contribution (EFC). This measures a family's financial capacity, determines how much federal aid a student is eligible for, and may be used by your state and schools to determine grant and scholarship eligibility.

When do I need to fill out FAFSA?

FAFSA for the next academic year becomes available on October 1. So, if your student is a rising senior and plans on attending college beginning with the 2025 fall semester, FAFSA will become available on October 1, 2024.

Many colleges have different FAFSA deadlines, so be sure to check each school’s financial aid office. If you’re not sure which schools you’re applying to, that’s OK—just list the ones you’re interested in. Different states also have different deadlines.

Officially, the U.S. Department of Education’s federal deadline to complete FAFSA is June 30; however, the sooner you submit your form, the better. Aim for December at the very latest.

Who should fill out FAFSA?

According to studentaid.gov, “The Free Application for Federal Student Aid (FAFSA) form is the student’s responsibility, but when a student is considered a dependent student for FAFSA purposes, parents have a large role in the application process.”

When filling out the form, it is important to identify who the student’s primary parent(s) are.

- Parents married to each other: report information for both parents on FAFSA.

- Parents who are unmarried but live together: report information for both parents on FAFSA, even if they were never married, are divorced or are separated.

- Parents who are unmarried and do not live together: if a student lived with one parent more than the other for the last 12 months, they should report that parent’s information on FAFSA. If they spent an equal amount of time living with each parent, they should report the information of the parent who provided more financial support over the last 12 months. If the reporting parent has remarried, also report information for the stepparent on the FAFSA form.

Per studentaid.gov, it is important to note that “dependent students are required to report parent information when completing the FAFSA form.” This includes biological and adoptive parents and legal guardians. Stepparents are considered parents if they are married to a biological or adoptive parent and if the student counts in their household size.

Students who were not dependents of their parent(s) or legal guardian(s) for the last 12 months should fill out the FAFSA form with their own information.

What do I need in order to complete FAFSA?

Parents and children should gather the following materials prior to completing the form:

- Social Security number, or Alien Registration number for non-U.S. citizens who are eligible noncitizens.

- Federal income tax returns, W-2s and other records of money earned.

- Bank statements and records of investments, if applicable.

- Records of untaxed income, if applicable.

To get started, one parent and the student must both create FSA ID usernames and passwords, which they will use to sign in. Students must also create a save key, a temporary password that enables them to return to partially completed FAFSA forms.

How do I complete FAFSA?

There are three options when it comes to filling out the FAFSA form:

- Log in at fafsa.gov to complete the form online.

- Complete the FAFSA PDF for the award year you’re applying for. In this case, you must print and mail the FAFSA PDF for processing.

- In some cases, schools may submit the FAFSA form for students.

Technically, the form is the student’s application, so where it says “you” on the form, it means the student.

You may use the IRS Data Retrieval Tool (IRS DRT) to transfer your federal tax return information into the FAFSA form. Once you submit your form, you will see a confirmation page and may also see a link to your state’s financial aid application. You may be able to transfer your federal information into the state application. Parents who have more than one child attending college can transfer their information to their other child/children’s FAFSA form(s).

What happens next?

You will receive a confirmation email that your FAFSA form has been submitted, processed, and sent to schools. You may check your application status online or by phone at 1-800-4-FED-AID.

After your application is processed, the student will receive a Student Aid Report. It is important to review this to ensure your information is correct and complete. Students typically receive federal, state and scholarship aid offers from schools in the winter and spring. studentaid.gov has great resources for understanding and comparing aid offers and what they mean for financing education.

Still need help? Visit Federal Student Aid for more information, tips and frequently asked questions.

5 minutes read

Finance

One goal that resonates with many Americans is becoming wealthy, although that means different things to different people—for some, it’s comfort and security, for others lottery-winner-level luxury. Get-rich-quick scenarios aside, for most of us, the key to making that wish for wealth a reality is disciplined saving and investing. In Part I of our Smart Money Goals post, the emphasis was on fundamental approaches to setting yourself up for future financial success. Now in Part II we delve into five tactics to help grow your affluence over time.

- Automate your savings

Accumulating savings is a precursor to investing. To ensure consistent contributions to your wealth-building journey, automate your savings. Through your employer or your bank, arrange automatic transfers of a portion of every paycheck into separate savings or retirement accounts. If your employer offers a 401(k) or similar plan, have your contribution automatically withdrawn from your paycheck and deposited into your account. Financial advisers recommend contributing at least enough to maximize your employer’s matching contribution in retirement plans.

- Reminder to rebalance

Out of sight is not out of mind. Even though your deposits are set up to operate without much input, it’s important to periodically revisit your accounts and adjust them as necessary. Schedule a quarterly, semi-annual or annual fine-tuning session.

- Bump up the savings rate

From time to time, boost your savings percentage, especially when you receive a raise or a bonus. These small increases can pay off over the long term. Take advantage of money market accounts that earn interest. If you won’t need access to your money for several months, CDs can be a good option.

- Invest for growth

While savings accounts offer security, inflation may outpace any interest you earn. For a greater payoff, you can put your capital to work with investments—a good place to start is with the basics: stocks, bonds and mutual funds. Since all types of investments perform differently, and investing carries inherent risk, spreading your capital around into diverse types of investments can be a sound tactic. Attempting to predict what’s going to happen with the stock market is risky. A safer approach is practicing discipline by staying invested in a diversified portfolio, even during downturns.

- Watch out for the fees

Different investments include different kinds of costs—expense ratios, custodian and maintenance fees, and loads and commissions are just a few. It’s worth educating yourself about what types of costs are associated with your investments, and to recognize that these costs that start out as a small percentage can add up fast, especially as your investment grows in value. Choosing lower cost purchases will soften the sticker shock.

Building wealth is a long-term goal: Earning interest and making wise investments puts your money to work for you behind the scenes, while you go on about your life. Strategic financial habits will help you pave the way and weather setbacks on your way to achieving financial success. Visit your local WaterStone Bank branch to speak with a banker and learn how you can start taking steps to building wealth.

3 minutes read

Finance

The journey to financial well-being begins with setting clear, attainable goals. These objectives will not only provide a roadmap for financial success but are also the building blocks for future stability. This two-part post covering short- and long-term financial goals begins with five actions that will set you up for financial success in the new year and beyond.

- Emergency Fund: Build or Replenish

Establishing or replacing an emergency fund is a crucial short-term goal. Aim to save enough to cover three to six months’ worth of living expenses. Consider housing, utilities, transportation, insurance and medical costs, among others. This fund serves as a safety net for unexpected expenses or sudden changes in your circumstances.

- Pay Off High-Interest Debt

Prioritize paying off credit card balances or personal loans. Reducing or eliminating debt not only improves your financial health but also frees up money that can be redirected towards other goals.

- Create a Monthly Budget

Develop a detailed monthly budget that accounts for all your income and expenses. Consider fixed expenses such as rent or mortgage payments, as well as variable expenses, such as grocery and food costs.

- Save for a Specific Purchase

Identify a short-term objective to save for, such as a vacation or a new electronic device. Working toward and achieving smaller goals can prove a sense of accomplishment and help you practice disciplined financial habits that lay the groundwork for greater aspirations, such as purchasing a house.

- Establish a Retirement Savings Habit

If you haven’t already, start contributing to a retirement savings accounts, such as a 401(k) or an Individual Retirement Account (IRA). While retirement is a long-term goal, initiating the habit of regular contributions is a crucial short-term step toward securing your financial future.

Remember that the key to achieving goals is setting realistic targets and tracking your progress, recalibrating as needed. For setting long-term financial goals, check out Smart Money Goals Part II.

2 minutes read

Finance

Ready or not, April 15 is coming! Whether you work with an accountant or do your taxes yourself, understanding the ins and outs can be a minefield.

Understanding tax deductions

One component of doing taxes that can be particularly confusing is the concept of tax deductions. A tax deduction is an expense that you can subtract from your income, reducing the amount you pay in taxes. Tax deductions lower your taxable income, helping you save money.

Charitable donations are the most common types of tax deductions as they reduce your taxable income by subtracting the amount of money you donated to charity. For example, if your annual income is $75,000 and you donate $3,000 to charity, you will be only taxed on $72,000.

Understanding tax credits

While tax deductions lower your taxable income, tax credits reduce the amount of tax you owe and cut your taxes dollar for dollar. Think about it this way—if you make $100,000 a year and have a tax deduction of $10,000, your taxable income is $90,000. If your tax rate is 25%, that’s a tax bill of $22,500.

Now, let’s say your income is still $100,000 a year, you don’t have any deductions, and your tax rate is 25%. That puts your calculated taxes at $25,000. However, you have a tax credit of $10,000, bringing your actual tax bill down to $15,000.

Tax credits can be either refundable or nonrefundable:

- Nonrefundable: If you don’t owe much in taxes, it’s possible that you won’t be able to receive the full value of your credit. For example, a $500 tax bill and $1,000 credit won’t get you a $500 refund check—it just means you’ll owe $0 in taxes.

- Refundable: Refundable tax credits include the earned income tax credit and the child tax credit. In these cases, if the value of your credit exceeds the amount you owe in taxes, you will receive a refund check.

Standard vs. itemized deductions

You have two options when it comes to tax deductions: standard deductions and itemized deductions.

- Standard deductions: The IRS sets the standard deduction each year, and it’s the easiest option, especially if you’re doing your taxes yourself. If you choose to go this route, your taxable income is automatically reduced by a set amount based on how you file (single, married filing jointly, etc.).

- Itemized deductions: With itemized deductions, you need to list each one of your deductions you’d like to claim ($50 to charity A, $100 to charity B, etc.). Itemizing can be a pain, but it’s worth it if you have enough deductions that will lower your taxable income more than the standard deduction.

Choosing the best option for you

How do you know whether a standard or itemized deduction is best for you? Standard deductions for 2023 are:

- Single: $13,850

- Married filing jointly: $27,700

- Married filing separately: $13,850

- Head of household: $20,800

Charitable donations aren’t the only things that are tax deductible. Other write-offs include:

- Medical expenses: expenses that are more than 7.5% of your taxable income and weren’t covered by insurance

- State and local taxes: the IRS allows people to choose whether or not they deduct state and local sales and income tax

- Student loan interest: even if you don’t itemize, you can write off interest paid on student loans

- Mortgage interest: you may deduct the interest you paid on up to $750,000 of mortgage debt

- Retirement and investing: traditional IRA contributions are tax-deductible, but your deduction might be limited

- Home office deduction: work-from-homers who set up a workspace used only for business can write off work-related expenses, including rent, utilities, and maintenance

The bottom line

So, which deduction is right for you? Most people take the standard deduction, but it can pay off—literally—to add up your itemized deductions before you make the final call. Would you save more by itemizing? Is the effort worth the time and payout, or is it easier for you to take the standard deduction and call it a day?

There’s no one-size-fits-all answer; it all depends on how complex your taxes are in a particular year. When in doubt, consult a tax expert who can point you in the right direction and help you better understand your individual tax situation.

3 minutes read

Finance

For many people, December is a time of reflection to look back on the past year and make plans for the new year ahead. Many people also resolve to make positive changes in their lives. In this spirit, the end of the year is the perfect time to take a look at a year’s worth of finances and make adjustments and plans for next year. (It also gives you a head start on tax season, which will be here before you know it!)

We’ve rounded up some top tips to help you check all the boxes on your end-of-year financial checklist.

Analyze your spending

How much money did you spend in 2023? Take a close look at all your accounts, expenses and bills to get a clear picture of how you allocated your spending. Did you take a bucket list vacation, funnel money into a college savings account, tackle a home improvement project, or just go out to eat a couple of times a week?

Also, consider any big life changes like marriage, divorce, a new baby, etc. Major life events can have a huge impact on your financial plan.

Once you have a solid understanding of your 2023 finances, see where you can adjust for 2024. That could mean spending less in certain areas of your life, increasing your regular contributions to a retirement account, or saving for a big purchase, like a new car.

Examine employee benefits

For most companies, benefits open enrollment falls toward the end of the year. This is a great time to review your current benefits, particularly retirement savings. For 2023, the maximum 401(k) contribution was $22,500, plus an additional $7,500 if you’re over 50. The maximum IRA contribution was $6,500, plus $1,000 if you’re 50+.

How did you stack up this year? Did you max out your contributions? Are you at least contributing as much as the employee match? If you can afford to, try to increase your monthly contribution next year. Also, look at allocations; are you satisfied with the ratio of stocks and bonds?

Many employee benefit plans also offer health savings accounts (HSA) and flexible spending accounts (FSA). Did you put any money into these accounts? How much of that money did you use, and what did you use it for? Remember: HSA contributions do not expire, but money in FSAs must be used by the end of the year.

Finally, now is a good time to update your beneficiaries and ensure your money ends up with the people you choose.

Prepare for tax day

April 15 will be here before you know it. Get ahead of the game by identifying any life events like marriage, divorce, births, deaths, and retirement that could affect your withholding status. An accountant can help you review any taxable transactions, deductible expenses, charitable gifts and more that might impact your taxes.

Review investments

Investing is a long game, but it never hurts to look at your allocations and determine if you’re getting the most bang for your buck. Are certain assets under- or over-performing? Are you comfortable with riskier investments, or are you ready for a more steady, conservative approach? Keep in mind that capital gains and investment losses can make a big impact on your taxes. When in doubt, speak to an investment professional who can help steer you in the right direction.

Assess charitable contributions

Charitable contributions aren’t just a nice gesture—they’re also tax deductible. Did you maximize your charitable contributions in 2023? Did you donate any assets, like a pre-owned vehicle? To learn more about charitable contributions and how they impact your taxes, speak with an accountant or tax advisor.

Manage debt

Debt is part of life, but it’s how you manage it that matters. Are you carrying any credit card debt? Student loans? Auto loans? The end of the year is the perfect time to take a close look at your debt, interest rates, loan positions and more. Have you made any progress paying things down (or, even better, off)? Are you able to consolidate any loans or negotiate for lower interest rates in 2024?

The key is to balance your financial goals, and that includes paying down debt.

Consider estate planning

Wills, trusts, and estate planning aren’t always the most comfortable topics of discussion, but that doesn’t mean they’re any less important. The end of the year is a good time to review these types of planning documents, particularly for beneficiaries and trustee designations. You may want to name a corporate trustee or co-trustee who can remain objective when administering a trust.

Ensure you’re insured

Last but not least, examine your insurance policies and coverage. Are you getting the most out of your policies? Are they still worthwhile? Is your coverage sufficient for your needs? As with estate planning, this is a good time to make sure your beneficiaries are up to date.

Still have questions about year-end financial planning? Contact WaterStone Bank for more information.

4 minutes read

Finance

The holiday shopping season has arrived, and with it an enticing array of discounts, sales, and specials. Everybody loves a good deal, but how can you be sure you’re getting the most bang for your buck? And how can you ensure you’re not falling victim to some retail mind control? We’ve rounded up some of the most common strategies that retailers use to bring in the big bucks at your expense.

Price Anchoring

Price anchoring is a psychological strategy that involves comparing two similar items, one at a high price and one at a lower price. The higher-priced option is used as an anchor to make the lower-priced product seem more attractive. You see this a lot in infomercials: “This product is normally $250, but if you order in the next 30 minutes, it’s yours for $50!” Avoid price anchoring by shopping around, comparing product prices and reading reviews.

Price Cushioning

Let’s say you’re shopping for sneakers, and you see one pair for $50, and another for $20. Most shoppers will opt for the more expensive pair, as they perceive them as being of higher quality. But if you throw a third pair of shoes into the mix at $35, suddenly that option seems much more appealing! It all comes down to how the options were presented to them. Avoid falling for price cushioning by figuring out exactly what you want and saving for it.

Buy One, Get One

BOGO offers seem like a great deal—after all, you're getting something for a much lower price, if not for free! But really, they’re just a trick of the trade to get consumers to buy two things, when they really only need one. Stores use this strategy to spend more money than you originally planned.

Coupons

Coupons can be tricky. Many times, store-brand items are cheaper than name-brand products—even with a coupon for the name-brand item. Other times, coupons come with a long list of restrictions. Or, what may seem like a great incentive (earn a $10 coupon for a certain amount spent) is just a tactic to get you to spend more at a later date.

Eye-Level Options

Why does it always seem like the best products are right at eye level? Because they are. Stores carefully position items so that the most enticing are at eye level, exactly where you’ll see them. Lower-priced and sale items are positioned below eye level or at the back of the store and are generally more difficult to find. Try to avoid “shiny object syndrome” and hunt for the good deals.

Sensory Appeal

Things like music to listen to, perfumes to smell, food samples to taste, etc. all enhance the senses and create a sense of urgency and desire. This sensory appeal helps people connect with individual products and encourages them to spend more.

Store Layouts

Have you ever noticed that when you walk into a store, there aren’t displays until you get about five steps in? That's because, psychologically, when people walk into a store, they’re trying to orient themselves. They don’t notice products right by the door because their focus is on where to go next. People also tend to move to the right first, which has caused many stores to create strategic layouts and navigational blockers that encourage shoppers to spend more. (Grocery stores and a certain Swedish home goods retailer have this down to a science!) Finally, people often perceive products placed on endcaps to be better deals, but that’s not always the truth. More often, they’re name-brand impulse buys.

Vanity Sizing

Anyone who has gone clothes shopping recently understands that sizing is drastically different from one store to another. You may fit into size 8 jeans at one store, and size 12 at another. This is called vanity sizing. Stores give customers a little ego boost by monkeying around with their sizes so that people keep coming back. There’s no easy way to avoid vanity sizing; instead, try on a variety of sizes at each store and buy what fits. The number is arbitrary!

Point-of-Purchase Displays

Point-of-purchase products are typically displayed throughout the line as you wait for your turn to check out. They’re those bright, shiny objects that you don’t need, but just can’t resist when you see them. Most stores have these, whether they’re last-minute snacks, new nail polish colors, seasonal items, etc.

Credit Card Offers

Many stores offer an immediate discount if you apply for their credit card. But what they don’t mention is the high interest rates that will negate your immediate savings, and how easy it is to rack up a balance. And don’t think that you can get off scot-free by applying for the card and canceling it later. That can actually do long-term damage to your credit score.

Free Shipping

How many times have you gone to check out while online shopping, only to find out that if you spend just $2 more, you’ll qualify for free shipping? Except that you can't find anything on the site that costs less than $10, which is more than the cost of shipping. Now, you could purchase those extra items and return them later, but is it worth it? And will you remember to do so? The retailer is willing to bet you won’t.

Limited Time Only

A sense of urgency and exclusivity encourages consumers to make impulse purchases while they can. After all, what if that cute sweater sells out? Another tactic online retailers use is a “1 item left” tag. This threat encourages you to purchase the item before someone gets to it before you. But in reality, there's no way to know for sure that it’s the only one left.

The age-old phrase is true: If something seems too good to be true, it probably is. Do your research, compare products and understand that some of these “deals” might just be a retailer trying to take you for a ride.

For more financial tips and tricks to save your hard-earned money, check out the WaterStone Bank blog.

5 minutes read

Banking

The holidays are here, and with them come tighter belts and tighter budgets. But that doesn’t mean you can’t eat like kings and queens this Thanksgiving! We’ve rounded up our top tips for festive feasting to ensure your day of thanks is delicious without breaking the bank.

Set a budget

Take a look at your food budget and decide what you can realistically afford to spend on your Thanksgiving meal. Where can you cut corners? Are there any foods that people barely touch that you can leave off this year’s menu? These days, many grocery stores have websites with prices listed; do your homework and stick to your list.

Research recipes

Every Thanksgiving table has the standards: turkey, mashed potatoes, stuffing and more. Before you head to the store to stock up, take a close look at your recipes and which ingredients you already have in your pantry. Do you need more cinnamon, or is there a jar hiding in the back of the pantry? Avoiding superfluous spending will help you stay on budget.

Make a list

We’ve all done it: We go to the grocery store without a list, thinking that we know exactly what we need. And how many times have you walked out without a key item, or added extra items to your cart? It’s easy to do! This Thanksgiving, make a list and stick to it.

Shop in season

When planning this year’s Thanksgiving menu, consider in-season, and therefore affordable, fruits and vegetables like apples, cranberries, squash, pumpkin, broccoli and more. Many of these are already Thanksgiving classics, so it’s a win-win!

Stock up where you can

To avoid dropping a chunk of change at one time, stock up where you can. Buy non-perishable items like wine, napkins and canned goods when they’re on sale, and remember that some perishable items, like potatoes, have longer shelf lives than others. Spreading out your spending makes Thanksgiving shopping easier to digest.

Decrease decor

These days, it’s easy to look at social media and think you need to go overboard with your decor, but it’s just not true. Thanksgiving is all about sharing a meal with the ones you love and being thankful for what you have—not trying to prove yourself for faceless followers on social media. Save money this year by repurposing existing decor, doing DIY projects with the kids, or bringing in touches from the outside like pumpkins and flowers from the garden.

Embrace potluck style

It’s usually easiest for the Thanksgiving host to cook the turkey, but that doesn’t mean they should be responsible for all of the sides. Save money this year by making Thanksgiving a potluck event and assigning sides and desserts to your guests. Not only does it save money, but it’s also a great way to try new dishes and flavors!

Love the leftovers

A big meal like Thanksgiving usually results in a lot of leftovers. Reduce food waste by sending leftovers home with guests, creating a casserole with your favorite dishes, adding fruits to muffins and oatmeal, and so on. The possibilities are endless, and there are countless recipes online to help you craft a delicious Thanksgiving leftover recipe that just might become a yearly mainstay.

During this season of gratitude, we’re thankful for customers like you. Wishing you a Thanksgiving filled with happiness and cherished moments with your loved ones!

3 minutes read

Finance

Temperatures are dropping, leaves are falling and everybody’s favorite autumn beverage—pumpkin spice—is back. As we begin to spend more time indoors, it’s a great time to think about renovations and home improvement projects to take on during the colder months.

Getting started

So, where to start? First, think about the scope of your project and what you’re trying to accomplish. Are you planning on cosmetic updates, like a fresh coat of paint and some new cozy blankets and throw pillows? Or do you want to install a gas fireplace, replace your kitchen cabinets or finish your basement?

Funding your project

If your renovation project is on the larger side, chances are you may want to leverage your home’s equity to fund it. Your home’s equity consists of the portion of your home that you own outright, whether that was paid in cash or via a mortgage. If you have paid off a significant portion of your home, you can use that equity to fund renovations—basically, using your home’s worth to increase its worth. One way to fund your project is through a home equity line of credit, or HELOC.

HELOCs are lines of credit that can have fixed or variable interest rates. You may access funds and make interest payments for a specific period of time (usually around 10 years); after that period of time ends, a repayment period begins, during which you may no longer access the funds.

Pros and cons of HELOCs

Pros:

- The freedom to use as much or as little money as you need, whenever you need it

- You are only obligated to repay the amount of credit you have used and pay interest on the amount you’ve withdrawn

- Ideal if you’re not sure how much time and money you’ll actually need to complete your renovation project

Cons:

- Interest rates may fluctuate, which means your monthly payments may increase

- You can borrow from a HELOC multiple times and don’t need to start paying back the principal right away, so it can be easy to accrue a balance

- Potential annual fees

- HELOCs factor into your credit report

Factors to consider

Before opting for a HELOC, it’s important to consider whether or not your home improvement project increases your property value and if you’ll see a return on your investment. This can be quantitative or qualitative. Quantitatively, a $25,000 kitchen remodel doesn’t necessarily mean your home’s value will increase by $25,000. However, qualitatively, a remodel may make your everyday life easier and add personal value.

It’s also important to consider your project budget, how much you can realistically afford to borrow, and how long it will take to repay it. If HGTV has taught us anything, it’s that renovations usually take longer and cost more than you anticipate.

Applying for home equity funding

The WaterStone Bank home equity line of credit has no minimum requirements on transactions, allowing you to spend what you need, when you need it. Easier access to your funds means greater financial control, coupled with flexible payment options.

Apply for a HELOC today!

4 minutes read

Security

In this day and age, it’s virtually impossible to escape the internet. We live in a digital world, and as great as it can be—information at your fingertips, ease of use, funny cat videos—it also has a dark underbelly. Over the years, scammers have grown more sophisticated and found new ways to access personal information you’d rather keep private. How in tune are you with common information theft scams, and do you know how to avoid them?

Spoofing and phishing

Spoofing and phishing are probably the most common scams—and the easiest to avoid. Email scammers try to catch your eye with an attention-grabbing subject line, whether it’s a problem with your bank account or a can’t-miss sale at your favorite store. When you click a link or open an attachment, the scammer installs malware on your device that can infiltrate your files and steal information like bank account numbers, website passwords and more.

Common email scams include:

- Scams that imitate a person or business you’re familiar with

- An urgent, don’t-miss-it offer

- An “official notice” that encourages you to take action

- Lottery win

- Fake survey

Phone scammers call claiming to be from a legitimate business and ask you to take action. They may request an additional payment so that an essential service, like your power, remains on. Or, they may call and ask you to verify a code that was sent to you via text message from a legitimate business.

How to protect yourself from falling victim to spoofing and phishing:

- Examine each email carefully. Do you recognize the sender, or is there something off about their name or email address? Look for things like a zero instead of an O, or an unusual number of misspelled words.

- Hover over links and images without clicking to see what shows up; does it look like a legitimate website, or does it have a string of characters that make no sense?

- If anything looks strange, err on the side of caution. Contact the supposed sender/caller directly to verify whether or not the email or call is legitimate.

- Most businesses will not call and request codes sent via text message. Anyone who calls should be considered suspicious.

Elder fraud

Elderly people are still the most likely to fall victim to scams. Take, for example, a woman who receives an email from her grandson, who is studying abroad and asks her to wire him money. On the surface, the facts check out; however, it’s possible that the grandson’s email account was hacked and that the email is a scam.

How to protect yourself from elder fraud:

- Double-check everything before taking action. Contact the individual or business that appears to have sent you the email or made the phone call to verify that it was them.

- Anyone asking for personal information should be considered suspicious, unless you are 100% sure that they are legitimate.

Unsecured passwords

There was once a day when we only needed one or two passwords for a handful of websites. Nowadays, you need a password for everything—and, yes, it’s smart to have a different password for each. It’s annoying, but it’s for your own good.

How to secure your passwords:

- Do not keep a doc on your device listing all your passwords. That’s the first thing a hacker will look for.

- Don’t use things like addresses, children’s or pets’ names, or any other identifying details in your password.

- Don’t comment on social media posts that pose a question for which the answer is somewhat personal. It’s an open invitation for scammers to guess your password and hack your social media accounts—or worse.

- Use a variety of letters and characters in an order that doesn’t make sense. Password! is probably the worst password ever. P@$$w0rd! isn’t great, but it’s better.

At the end of the day, an ounce of prevention is worth a pound of cure. If something seems too good to be true, or sounds a little fishy, it probably is. Double-check everything, follow your instincts and don’t keep your passwords in a digital file on your computer.

Remember, WaterStone Bank will never call or email you directly and ask for your personal information. If you have questions or believe you may have fallen victim to a scam, please call our Customer Support Center at (414) 761-1000, or visit your local branch immediately. For more security tips and additional resources, visit wsbonline.com.

5 minutes read

Finance

The holiday season is the most wonderful time of the year. From decorating your home and scoring that elusive toy atop your kids’ list, to baking cookies and partying until the ball drops, there is nothing quite like it. But all those festivities add up—literally. Now that Labor Day has passed, the holidays are right around the corner, which means it’s a great time to look at your holiday budget.

Here are our favorite holiday budgeting tips to help you avoid any surprises this season.

Set an overall budget

Take a look at your normal monthly budget and determine how much you can afford to spend on gifts for the holidays this year. Maybe you’ve been saving all year, or maybe it’s a bit of a squeeze. Whatever your situation, figure out how much you plan to spend and then stick to it.

Set a budget per person

Chances are, you’ll probably spend more on gifts for your significant other and kids than you will on coworkers and friends. Break down your overall holiday budget and allocate an amount per person. It’s OK to give yourself a little bit of wiggle room just in case you find a stocking stuffer you know someone will love. Just don’t go overboard!

Avoid impulse buys

As the holiday season approaches, more and more retailers offer discounts and coupons you don’t always see throughout the year. These deals are great, as long as what they’re selling is something that is on your list. But try to avoid buying stuff just because there’s a discount. All those purchases add up!

Shop around

It literally pays to shop around. Unless an item is exclusive to a particular retailer, like an iPad, there’s a good chance you can find it at several different stores. Take a look at different sites to see who has the item on sale, who’s offering a discount, who has it in stock and who can ship it (even better if it’s free shipping!).

Consider non-gift expenses

Budgeting for gift-giving is obvious, but what about other incidental purchases, like replacement lights for the Christmas tree or baking supplies? It’s important to factor these into your budget, too.

Plan for the new year

Reviewing your bills after the holidays can be a bit of a gut-punch. You may find yourself a little strapped for cash in the new year, but planning now will help ease the blow later. Plan to take it easy in the new year by eating in, planning at-home date nights and other inexpensive but enjoyable activities. Your presence is the present!

For other holiday shopping tips, check out these blog posts: Best Tips for Getting a Jump Start on Holiday Shopping and Black Friday Shopping Tips: Is it Worth the Hype. And, if you’re looking for a one stop gift shop, know that your local WaterStone Bank branch is a great resource – from Visa gift cards to foreign currency, or membership for your littles in our Blue’s Jr. Bankers Kids Club.

Ultimately, when it comes to budgeting and holiday gift-giving, it really is the thought that counts. Budgeting is the smart choice and will make your holiday season that much more festive.

3 minutes read

Banking

Buying a home is a huge undertaking. There are so many things to consider, from budget to square footage, school district to number of bedrooms. But there’s one thing that stands above the rest and is crucial to making the actual purchase: the mortgage. There are several types of mortgage loans, and we’ve broken each one down to help you make an informed decision.

Fixed-rate loans

Fixed-rate home loans are the most common types of mortgages. Your interest rate stays the same, whether you pay off your home in 15 years or 30. Even if the market rates change, you’re all set—you’ve locked in a rate. However, your overall monthly payment may fluctuate depending on changes to property taxes and home insurance premiums.

If your down payment is less than 20%, many lenders require home buyers to purchase private mortgage insurance (PMI). PMI protects lenders in the event that homeowners are unable to make their monthly payments. It does NOT protect the buyer. However, most buyers are permitted to cancel their PMI once they’ve reached 20% equity in their home.

Adjustable-rate loans

Contrary to fixed-rate mortgages, adjustable-rate mortgages have interest rates that change over time. They start with an introductory period – the length varies by lender. Buyers can count on fixed interest rates that are generally lower than the current market rates.

Then comes the adjustment period, during which interest rates vary over time. Many lenders put caps on how much rates can rise and fall over time.

Conventional loans

Conventional loans are mortgages offered by private lenders. Though it’s possible to get a conventional loan with just a 3% down payment, they lack government backing and usually come with stricter requirements for borrowers, like minimum credit scores of 620 and a debt-to-income ratio of less than or equal to 50%.

FHA loans

Federal Housing Administration (FHA) loans are government-backed loans that are offered through private lenders. These types of mortgages help buyers with lower credit scores purchase homes. However, it’s important to note that people who opt for an FHA loan need to pay mortgage insurance premiums up front, as well as a monthly mortgage insurance premium. Unlike PMI, you can’t cancel these over time; you must continue to pay them until your home is paid in full.

VA loan

VA loans come straight from the Department of Veterans Affairs and are offered exclusively to U.S. veterans, active-duty military and, in some cases, surviving spouses. Borrowers must provide a certificate of eligibility and meet other qualifications.

USDA loan

U.S. Department of Agriculture (USDA) loans are great options for people who plan to buy homes in rural areas. Properties must meet USDA requirements and borrowers must meet USDA income limits.

Nonconforming loans

Most mortgages are conforming loans, which are almost immediately purchased by Fannie Mae or Freddie Mac. Nonconforming loans, like jumbo loans, are high-value loans that exceed the Federal Housing Finance Agency’s loan limits. They’re more common in expensive metropolitan areas and have stricter requirements for borrowers.

Which loan is best for you?

The type of loan that is best for you depends on your financial situation, like how much money you can put down on your house, what amount you prequalify for, your credit score and much more. Meet with our Residential Mortgage Loan Officer, Peter Salamone, to learn more about the right option for you. Give him a call at 414-459-4579 or email him at petersalamone@wsbonline.com.

4 minutes read

Finance

Going off to college is an exciting time—newfound independence, solo decision-making and lots of fun. But with this new stage in life comes new responsibilities. No one is looking over your shoulder to ensure you do your homework, you don’t have to check in with mom and dad before you go out, and nobody is managing your spending—which is precisely why you, as a student, need to.

Budgeting may not be glamorous, but it is an important part of being an adult. And the earlier you learn how to create and stick to a budget, the better off you’ll be in college and beyond. Here are our top tips for budgeting as a college student.

Keep track of your spending

Make a list of your fixed expenses, like your cell phone bill, rent, internet—anything that is the exact same amount each month. Then, take a look at your variable expenses, like eating out, going to the movies, and any other expense you can’t necessarily predict. It’s important to know where your money is going, what you can afford, and where you can cut corners.

There are lots of digital tools and apps to help track your finances and make it easy to budget.

Set goals

We wouldn’t be surprised if you haven’t thought much about your long-term financial goals, beyond getting a job and supporting yourself after graduation. Setting goals can help create a blueprint for your future, including paying off student loans, saving to buy a car or house, or just moving out of your parents’ house.

It’s possible your goals may change over time, but the earlier you start making them, the better.

Consider credit

The concept of credit can seem like walking a tightrope—you don’t want to rack up a big credit card bill, but building credit is important. A healthy credit score will serve you well in the future, when it comes time to buy a house. Start by choosing a credit card wisely; pay attention to fees, interest rates, and incentives. Then, make a herculean effort to keep your balance as low as possible—don’t order pizza willy-nilly, don’t go on any unnecessary shopping sprees. In addition to keeping your balance low, it’s also crucial to do your best to pay your bill on time every month (and paid in full, if possible).

It’s easy to put things on a credit card here and there, but you’d be surprised how quickly the balance grows.

Get a job

Many college students are eligible for work-study programs through their school. If you weren’t able to land a spot on campus, try looking nearby at a coffee shop, grocery store or any other business that offers part-time hours to students (there are always a ton near college campuses!). Keep some money to have fun with, and sock away the rest. You’ll be glad you did someday!

Live below your means

This is true of life in general. Many people have a champagne appetite on a beer budget, but the smart ones don’t spend money on things they can’t afford. As a rule, you should bring in more money than you spend. Overspending can lead to burst budgets and high credit card balances.

Apply for scholarships

If you already have scholarships through your school or outside sources, that’s great! It never hurts to keep looking, though, especially after you choose a course of study. Many scholarships are directed toward students in specific programs, so it pays off—literally—to keep an eye on things.

Save, save, save

Whenever you can save money, do! Every little bit counts, and you’ll be glad you did if and when times are tight. Plan ahead and you’ll be better set for your future!

And, if you’re looking for a checking account, savings account, or simply advice on the next steps in your financial journey, schedule an appointment, or stop by one of our convenient locations. At WaterStone Bank, we’re here just for you.

3 minutes read

Security

Many people use a computer on a daily basis for a variety of tasks such as online banking, working, and storing sensitive information. Recently, scammers and hackers have been intensifying their methods of obtaining your information fraudulently, making it harder to recognize before you become a victim. Staying vigilant online and being aware of certain scam tactics allows you to effectively protect your personal information, computer, and finances.

What is a Virus?

A virus is a small piece of malicious software that is connected to real programs or e-mail attachments. Viruses are virtually undetectable until the user downloads and opens the attachment. The computer becomes infected very quickly -- sometimes without the user even knowing, and all the data stored is now visible to the hacker.

What is Malware?

Malware is a certain type of virus that performs a variety of unwanted functions on the user's computer when infected. When malware is downloaded, pop-up ads may be shown, your e-mail may be spammed with unsolicited messages, and your internet activity may be logged and recorded for the hacker to discern.

What is Ransomware?

Ransomware is similar to malware in the sense that it can be unknowingly downloaded onto a computer by opening unsolicited e-mail attachments, downloading pirated software, or even viewing websites with embedded malware. Once ransomware is downloaded, the stakes intensify as it loads an encryption code onto the computer, ultimately locking access to either certain data or the computer itself. The hacker responsible will not remove the encryption until a ransom fee is paid. Businesses with weak cybersecurity systems continue to be the highest target of ransomware attacks, resulting in temporary or permanent loss of sensitive information, as well as extensive financial losses.

What are some preventative measures to take when recognizing scams?

Staying vigilant and recognizing warning signs is your best defense against scammers. Knowing how these scams work and the signs to look for will enable you to act before it's too late. Additionally, there are some extra precautions you can take to ensure comprehensive computer security.

- Always pay close attention to unknown attachments and e-mail messages and report any suspicious messages immediately.

- Avoid downloading pirated music, movies, and video games.

- Back up your computer data regularly, preferably to an external disk or hard drive.

- Do not click on unsolicited links or ads in e-mail messages or unsecured websites.

- Utilize anti-virus and anti-spyware software. Make sure they are set to automatically update and run regular scans.

- Carefully read End User Agreements before clicking accept. Be aware of the phrase "Third party software may be installed".

- Report all fraudulent activity to The Federal Trade Commission or The FBI Internet Crime Complaint Center, even if a scam was only attempted.

Remember that WaterStone Bank will not call you directly and ask for your personal information. If you have any questions or believe you may have fell victim to a scam, please call our Customer Support Center at (414) 761-1000 or your local branch immediately.

3 minutes read

Security

As businesses across the country continue to adjust their operations, many companies are maintaining remote work setups for their employees.

Working remotely presents new challenges for any team, especially when it comes to security. In order to protect your company's confidential information as work extends beyond the traditional office space, keep these guidelines in mind.

1. Secure your home networks.

Home internet networks don’t usually have the same rigorous security settings as office networks. As a remote employee, it is crucial to properly secure your home networks with encryption and password protection. Home networks should also have a unique name that doesn’t contain any personally identifying information.

Additionally, consider that if multiple devices are connected to your home network, such as streaming services, phones and other family members’ laptops, this could slow down internet speed during the workday.

2. Avoid using work devices for personal tasks.

As employees adjust to working remotely, the lines between work life and home life might start to blur. You should refrain from using work-issued devices for personal activities like checking social media, watching streaming sites, online banking, or online shopping. To keep sensitive company information and passwords secure, remote employees should only use their personal devices for these activities.

For extra protection, make an effort not to reuse your personal passwords on work accounts and follow best practices for creating secure passwords.

3. Take extra precautions with confidential information.

If you work with sensitive data such as bank account numbers, social security numbers or other personally identifying details, it's advisable to securely store physical documents in a locked cabinet at the end of each workday. Keep laptops, phones and other work devices password protected, and remember to log off whenever you walk away from your screen.

Sensitive information should only be accessed from a work-issued device—ideally from a secure VPN (virtual private network) or a company-approved cloud service, rather than a local device. Always communicate with your company's executives and IT department to determine what software is best for you.

3 minutes read

Finance

Any time you start a new chapter, it can feel overwhelming—especially if you’re a recent grad and just starting out in life as an independent adult.

Managing your finances can also seem intimidating when you’re first starting out. Between budgeting, saving, and investing, it’s easy to feel adrift amid all the information and advice.

Whether you’re recently out of school or you’re simply turning over a new leaf in life, a few simple steps can help put you on a path to financial security. Here are some key places to focus for anyone just starting out—or anyone ready for a new financial beginning.

- Start saving early for retirement.

Retirement may feel like a lifetime away, but the earlier you start saving for retirement, the better.

A recent survey found that 70 percent of retirees would tell their younger selves to start saving earlier, and for good reason: There are lots of benefits to saving early in your career, like being able to make post-tax contributions to a Roth IRA and take advantage of compound interest, which is when your initial investment grows exponentially as interest accumulates over the decades.

Even starting small—think $20 a paycheck—adds up to a solid savings. Online retirement savings calculators can help you visualize how a small investment in your early 20s can eventually grow into a large nest egg by the time you retire.

- Build up your emergency fund.

You never know when life will throw a wrench in your plans. From car breakdowns to temporary unemployment, there are countless situations that could arise when you least expect them.

Make sure you’re ready for the unexpected by starting to build up an emergency fund. There are lots of ways you can contribute to an emergency fund, including automatic deductions from your paycheck—a great way to “set it and forget it” and hold yourself accountable to saving—or lump-sum contributions, like depositing your yearly tax refund into savings.

- Create a budget.

Tracking your spending, tabulating expenses, and calculating monthly income may not seem too exciting. But the benefits of budgeting are plentiful, from helping you save and achieve your money goals to putting you in the driver’s seat of your finances.

A sense of control over your financial situation is crucial for starting out on the right foot as you get established. A budget can help you understand what you can comfortably afford and which purchases are out of reach. This ultimately empowers you to make informed decisions about your spending and avoid trouble down the road.

Luckily, there are lots of free tools online to help you create a budget, so you don’t have to start from scratch. If you’re not sure how to get started, search for tools and worksheets that lay out the basics of budgeting.

- Use credit wisely.

You may be wary of credit cards, especially if you’ve witnessed how credit card debt can become crippling. But “credit” isn’t a dirty word—it’s important to use it wisely as a tool in your financial quiver.

Opening a credit card that you pay off in full each month can help you build a good credit score, which will help you if you ever want to qualify for loans and competitive interest rates in the future. This becomes important if you ever hope to purchase a car, a home, or make other large investments.

Credit cards can also offer practical benefits and perks, like cash back on purchases or rewards on gas and travel expenses. Just be sure to avoid opening a card that charges an annual fee, and don’t use credit cards to make purchases you can’t afford.

4 minutes readBanking

Congratulations! The kids are grown and have moved out, and you’ve officially achieved empty-nester status. This is a great time to start planning for the next chapter of your life, whether that means downsizing, retirement, or both. However life may look, below are some essential tips to help empty nester navigate the downsizing journey with confidence.

Take a fresh look at your budget

Now that your kids have left the nest, your monthly budget likely looks very different (Has that grocery bill gone way down?). It’s a good time to take a fresh look at your budget and determine what your monthly expenses look like. Several may decrease, like utilities, and you may be able to cut some costs (like that streaming service that only the kids used).

But that doesn’t mean every expense will decrease. You may find that you spend more time going out to dinner, traveling, or taking up new hobbies. Or, your kids may still need financial assistance from time to time. Try to work these costs into your budget so that there are no surprises.

Pay off debt and keep saving

If you find that you have extra money each month, do your best to pay off debt first. There's some debate about how to go about this; some people start by paying off the balances that carry the highest interest rates. Others use the waterfall method and pay off smaller balances first, then put that money toward the next bill.

It’s also smart to start funneling as much money into savings, a 401(k), or IRA. The more you save now, the better; you’ll be glad you did when you retire.

Plan for retirement

Speaking of, retirement probably isn’t too far off. Hopefully, you’ve been contributing toward a 401(k) or IRA. Take a look at what percentage of your income goes toward retirement and consider increasing it, if you’re able. Individuals are permitted to contribute $6,500 annually toward an IRA; people age 50 and older may contribute an extra $1,000 each year.

Downsize your home

Whether or not to downsize your home depends on where you see life going. Do you anticipate having grandchildren and hosting big holiday celebrations? Or are you ready to scale things back and move into a condo? Consider what living situation is right for you, like access to medical care, weather, taxes and more.

Create an estate plan

Most people draw up estate plans when they start having kids, and most don’t look at them carefully afterward. This is a great time to review your plans and make changes depending on where life has taken you. You no longer need to worry about who will serve as guardian of your children, but you may want to think about how to split your assets among your children, who will serve as the executor of your estate and who will benefit from insurance policies.

Think about what’s next

If you’re not already retired, think about how long you’d like to continue working. Perhaps you and your partner would like to plan your retirement so that you stop working at the same time. Consider the financial ramifications; can you afford to retire? Will you need to take on a post-retirement, part-time job? How will you fill your time after you retire? Thinking about this will help you plan for the future.

Give yourself some grace

Becoming an empty nester is a big life change. Some people are ready for it, and some grieve their baby birds flying the coop. Be kind to yourself; spend more time on your hobbies, make new friends or plan a date night. Things are different, but different is good. And remember—you’ll always be a parent. Your kids will always need you.

However the planning for your next stage of life may look, WaterStone Bank is here just for you when it comes to your finances. Give us a call, schedule an appointment, or stop into one of our branch locations.

3 minutes read

Banking

You can do all the right things—make and stick to a budget, watch your spending, put money into savings—and unexpected expenses will still crop up. But with a little planning, you’ll be better prepared for whatever life throws at you.

Create an emergency fund

An emergency fund is something you can rely on when the going gets tough. There’s no set amount to strive for, but most people try to have three months’ worth of expenses socked away for a rainy day. Make a goal and try to save money each month. Better yet, use online banking to set up automatic deductions from checking into savings.

Take a closer look at your spending

Make a list of all of your monthly expenses: rent/mortgage payment, gasoline, internet, cell phone and so on. What can you afford to cut back on—or cut completely? Is there a certain streaming service you only use once in a blue moon? Can you rent audiobooks from the library rather than purchasing them with a paid subscription? It doesn’t have to be forever, but little cuts here and there can make a difference in the long run and help you save.

Take on a side hustle

We’re not saying you need to juggle two full-time jobs, but a side hustle can help you bring in a little extra income. Maybe you love making jewelry—can you sell your creations on Etsy? Are there any freelance gigs you can take on? How about pet sitting or dog walking? Put any extra money you earn into your emergency fund so it’s there when you need it.

Negotiate with credit card companies

If you carry a credit card balance, you already know that interest rates can be a beast. Contact your credit card company to ask about lowering your interest rate or monthly payments and erasing late fees. It won’t eliminate your debt, but it’ll make things easier to manage until you’re back on your feet.

Look into short-term loans

Short-term personal loans can help cover your expenses and tide you over in the short term. They are not meant to be a long-term solution and should be paid off as soon as possible. Review the loan terms carefully and double-check the fees and interest rates—some of which may be significant.

Ask your employer about a paycheck advance

Some employers offer paycheck advances for work you’ll do in the future. Contact your human resources department to find out if it’s something your company offers.

Shop for insurance

Insurance is a great safeguard in an emergency. Take some time to review your policies and shop around. Could you pay less for the same—or better—coverage with another company? Do you really need that extra life insurance policy? Shopping around is a great way to reduce your spending.

The bottom line

No matter how you choose to prepare for unexpected expenses, it’s important to take whatever money you save and funnel it into your emergency fund. Every little bit counts, and you’ll be surprised how quickly it adds up. And if or when the day comes that you need to dip into your savings, you’ll be glad you began saving when you did.

Schedule an appointment today to meet with a banker and discuss the best options for your emergency fund. At WaterStone Bank, we’re here just for you!

3 minutes read

Finance

Road trips are a mainstay of the summer vacation circuit. The great part about living in the Milwaukee area is that you’re within driving distance of tons of favorite locations across the Midwest. In Wisconsin alone you have “Up North,” Door County, Madison and, of course, Wisconsin Dells. But you’re also within an easy drive of other happening cities like Chicago, Minneapolis/St. Paul, St. Louis, Nashville, Mackinac Island, Niagara Falls and many more.

But, if you’re looking to leave the Midwest in your rear-view mirror, you’re in luck. There are plenty of road trips across the country that make for an excellent adventure.

- Route 66: The original route spanned 2,448 miles from Chicago, going through Missouri, Kansas, Oklahoma, Texas, New Mexico and Arizona before ending in Santa Monica, California. These days, you don’t have to drive the full stretch, but there are plenty of things to see and do along the way, wherever you choose to begin and end.

- Kentucky Bourbon Trail: With 37 distilleries to choose from, this is a great road trip for bourbon connoisseurs. Each distillery tour takes about 90 minutes, so unless you’re determined to visit them all, it’s probably best to pick a few. Pace yourself!

- The Lincoln Highway: The Lincoln Highway was the first transcontinental road for cars in the U.S. It crosses 13 states, beginning in New York City and ending in San Francisco. The route isn't what it was 100 years ago (many roads don’t exist anymore), but it’s easy enough to follow. Highlights include Times Square (New York), the Ten Millionth Model T (Ohio), Abraham Lincoln’s log cabin (Indiana), Lincoln monument (Wyoming), “the loneliest road in America” (Nevada) and the original Donner Pass—yes, those Donners (California).

- Columbia River Highway: About 75 miles long, this scenic highway runs from Oregon’s Troutdale to The Dalles. A highlight is Multnomah Falls in the Columbia River Gorge.

- Blue Ridge Parkway: A great budget road trip, this route spans 469 miles and passes through Virginia and North Carolina along the Blue Ridge Mountains.

- Great River Road: This collection of roads span 10 states (Wisconsin, Iowa, Illinois, Missouri, Kentucky, Tennessee, Arkansas and Mississippi) and ends in Louisiana. Stops along the way include St. Louis, MO; Elvis Presley’s home, Graceland (Memphis, TN); and New Orleans, LA.

- Pacific Coast Highway (PCH): OK, this one might be on the more expensive side, but what it lacks in budget-friendliness, it makes up for in spectacular views. The 1,650-mile PCH, also known as Highway 1, begins in San Francisco and winds along the California coast before reaching its final stop of San Diego. Must-see cities along the way include Monterey, Carmel-by-the-Sea, Big Sur, Solvang and Los Angeles.

Whether your travels take you near or far, your WaterStone Bank account is just a click away with Digital Banking. Wherever you’re headed this summer, we wish you safe travels!

Sources: The Travel, Lincoln Highway Association,

2 minutes read

Security

Over time, online scammers have become more sophisticated. It used to be easy to identify a scam—like the Nigerian prince who emailed everyone, asking for money. Now, online scams are easily disguised and have hoodwinked even the most tech-savvy folks. So, how can you protect your information and avoid falling victim?

A great starting point is to understand the most common scams and how they operate, as each type is engineered to gather information in a different way. Some of the most common scams include:

Phishing scams: Phishing scams are generally emails that appear to be from reputable sources, like banks, or online shopping sites. They trick you into clicking a link in the email, which installs malware on your device. Sometimes, scammers take things a step further and hold your information hostage, demanding a ransom payment for the safe return of your data. Tip-offs that an email might be a phishing scam include an urgent tone, misspelled words, and over-the-top threats, like financial consequences.

Pop-up scams: Also known as scareware, pop-up scams are fraudulent messages about fake antivirus software, tech support, and other services that claim your device or personal information has been compromised. When you click the link, hackers install malware that steals your information. Signs of scareware include popups that are difficult to close, urgent messaging, and software companies that sound made up.